Jan.2019

2019-02-20 20:34:40

China Textile 2019年2期

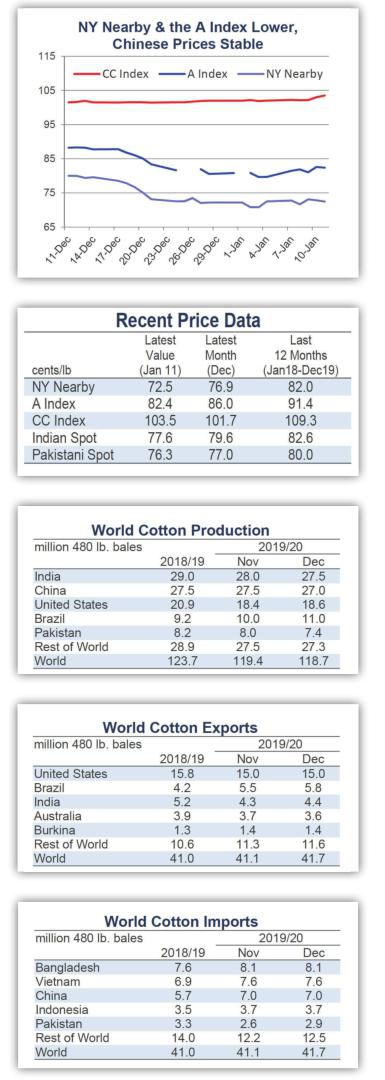

Recent price movement

NY futures and the A Index decreased throughout December before stabilizing in January. Chinese and Pakistani prices were stable over the past month. Indian prices moved slightly lower.

? The Nearby NY futures contract(March) fell from levels near 80 cents/ lb in early December to values as low as 70 cents/lb in January. In later trading, prices have been generally holding near 72 cents/lb.

? The A Index followed the same general pattern as NY futures. Values decreased from those near 88 cents/lb in early December to those just below 80 cents in early January. Recently, levels have been near 82 cents/lb.

? The Chinese Cotton Index (CC Index 3128B) was steady in both international (102 cents/lb) and local terms(15,400 RMB/ton).

? Indian spot prices (Shankar-6 quality) edged slightly lower over the past month, declining from 80 to 77 cents/lb or from 44,400 to 42,800 INR/candy.

? Pakistani spot prices were steady, trading between 76 and 77 cents/lb or from 8,700 and 8,800 PKR/maund over the past month.

Supply, demand, & trade

Due to the partial shutdown of the federal government that began on December 22nd, no updates were made to USDA supply and demand estimates this month. Although there are some govern- ment agencies that continue to release data as scheduled (for example, the employment and inflation figures issued by the Bureau of Labor Statistics), the majority of USDA statistics are not being published. Without revised estimates for January, this edition of the Monthly Economic Letter presents the same figures as last month (USDAs numbers from November and December).

Beyond supply and demand updates, another important stream of information from the USDA that has been interrupted is the weekly export sales and shipment data. In addition, U.S. trade data, which cover flows of fiber, yarn, and finished textile goods have been suspended.

Price outlook

The interruption in USDA revisions to supply and demand figures comes at an uncertain time for the market. Before its onset, 2018/19 could have been identified as a year of transition. Change implies uncertainty, and even though we are nearly halfway through the crop year, more questions than answers appear to be presenting themselves.

What had been expected to delineate 2018/19 from the past several crop years was that Chinas policies for drawing down reserve stocks would evolve into a policy of stabilization. Due to the reduction in government supplies over the past three years, Chinas ability to fill its production gap through the auction of reserve stocks has diminished. Correspondingly, it has been expected that China would need to increase imports. However, thus far, a definitive uptick in Chinese imports has yet to surface. There are seven months remaining in 2018/19 and it is still possible that Chinese imports could climb after the Chinese harvest is committed and mill inventories possibly start to decrease.

One factor that has not been supportive of rising Chinese imports is the lingering trade dispute between the U.S. and China. Officials from the U.S. and China met during the week of January 7th. After the meeting, it was reported that progress had been made, but no specific points of agreement were released and there was no mention of anything suggesting that China would buy more U.S. cotton (after negotiations in December, China did buy more U.S. soybeans).

Another factor inhibiting import demand and adding to uncertainty is the weakening global economic outlook. Since the summer, forecasts for global GDP have been adjusted lower. A chief concern is the slowdown in China and slow growth in Europe. In the U.S., the labor market remains strong, but there are a few indicators that suggest growth in the U.S. may have reached a peak (e.g., housing sales have slowed, inversion in interest rate yield curves).

Slower global economic growth is associated with slower demand growth. This is true across commodities, with the sharp declines in oil prices since October partially attributed to expectations of slower economic activity in China. Re-garding the USDAs current (December) set of cotton estimates, a common criticism is that their mill-use figure is too high and does not fully integrate the recent deterioration in macroeconomic conditions.

As we approach the timeframe when early estimates for the 2019/20 crop year are released, the threat of a recession at some point in the next year or two will be a source of uncertainty. While a downturn in economic growth suggests slower growth in mill-use, it should also be remembered that most recessions are not as severe as the one that occurred in 2008/09.

On the other side of the balance sheet, most preliminary discussion for 2019/20 production calls for relatively large increases. Across the worlds largest cotton growing countries, there were weather-related challenges this season. The U.S. suffered drought in West Texas in the spring and summer, the Southeast region was hit by a pair of hurricanes, and virtually all of the cotton belt was plagued by wet weather throughout the harvest period. Australia suffered drought. Northern India, Pakistan, and Central Asia suffered from below average streamflow out of the mountains for irrigation. In combination, these issues weighed on global production in 2018/19. More beneficial growing conditions in 2019/20 could result in a much larger global harvest.

Conditions have already turned favorable for 2019/20 production in West Texas. With plenty of rain in recent months, drought has been eradicated from the region, and ample soil moisture should be in place at the start of the season. Due to assumptions of lower abandonment and higher yields, the USDA issued a forecast in November suggesting that the U.S. could grow 22 million bales next crop year. Figures from private forecasters have been even higher, near 24 million bales. Improved growing conditions in other countries could add a million or two bales in several locations (e.g., India and Australia). Acreage could increase meaningfully in Brazil.

At a recent cotton conference, the USDA floated unofficial early estimates for 2019/20 which suggested the global increase in production could be 10.5 million bales. If realized, this suggests a record global crop next crop year (129.2 million bales). If so much cotton is grown, the possibility of a recession becomes all the more important for prices. A possible downturn in demand paired with a potential record harvest present the risk of a sizeable accumulation of stocks.

- China Textile的其它文章

- High quality development of Keqiao dyeing and printing industry

- Lenzing expands offering for nonwovens in a high-tech application facility

- Passing on the know-how at the Monforts production site

- Cotton production continued to grow rapidly in 2018

- The long view for ring spinners

- Forecast of Fabrics China Trends by Keqiao for the first time